.png)

The Insurance Email Problem

Insurance companies process millions of customer emails annually, and roughly 80% follow predictable patterns: claims status inquiries, renewal questions, policy coverage clarifications, and certificate of insurance requests. Yet most insurers still route every email through human agents because of compliance concerns.

Claims status inquiries represent 30–35% of volume. Renewal and billing questions account for 20–25%. Policy coverage questions make up 15–20%. Certificate of insurance requests represent 10–15% (particularly heavy in commercial lines). General account management adds another 10–15%.

What Makes Insurance Email AI Different

Policy Language Precision

Insurance policies are legal contracts. When a customer asks whether their homeowner's policy covers water damage from a burst pipe versus flooding, the answer has legal consequences. The AI must reference the specific policy language for that customer's contract, not generic descriptions. This requires integration with the policy administration system.

State-by-State Regulatory Variation

Insurance is regulated at the state level. Cancellation notice requirements, grace periods, claims handling timelines, and mandatory disclosures all vary by state. The AI must apply the correct regulatory framework for each policyholder automatically.

Claims Handling Sensitivity

The insurer has a duty of good faith. AI responses for claims must be factual and empathetic, never implying a valid claim will be denied. When in doubt, the AI must escalate rather than risk a response that could be construed as a coverage determination.

High-Automation Categories

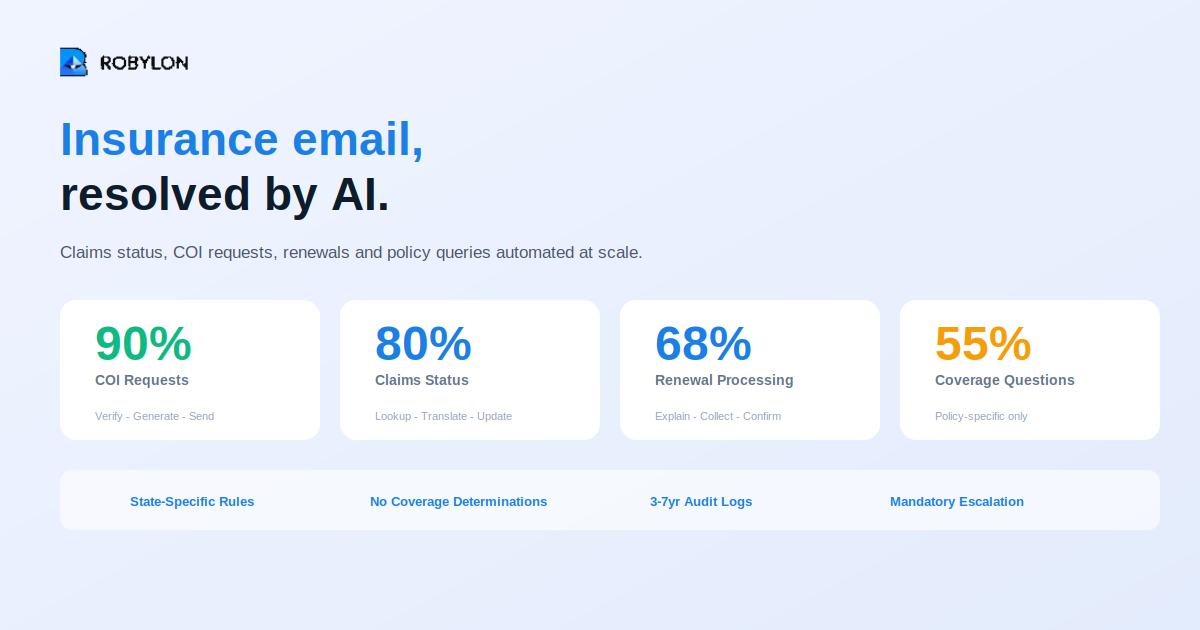

Claims Status Updates (75–85% automation)

The AI connects to the claims management system, identifies the claim, translates the internal status code into clear customer language, provides expected next steps and timeline, and includes the adjuster's contact information.

Certificate of Insurance Requests (85–95% automation)

COI requests are the easiest to automate — the AI verifies the policy is active, generates the certificate with the correct holder information, and sends it as a PDF attachment. This alone saves dozens of agent hours per week in commercial insurance.

Renewal Processing (60–75% automation)

The AI can explain premium changes by referencing specific factors, process renewal payments, and make routine coverage updates. Complex renewal negotiations require human handling.

Policy Coverage Questions (50–65% automation)

The AI retrieves the customer's actual policy, identifies relevant coverage sections and endorsements, provides the information with appropriate qualifications, and includes a disclaimer that the policy document governs.

Integration Architecture

Essential connections include policy administration system for real-time policy details, claims management system for status data, billing and payment systems, document management for COI generation, and regulatory compliance database for state-specific rules.

Compliance Guardrails

Never allow the AI to make coverage determinations. Include state-mandated disclosures in every relevant response. Log all interactions for regulatory examination (3–7 year retention). Implement mandatory escalation for emails mentioning attorney representation, department of insurance complaints, bad faith allegations, or fraud indicators.

Measuring Performance

Track claims email turnaround (from 24–48 hours to under 2 hours for status queries), COI generation time (from days to minutes), renewal retention rate, compliance audit results (zero violations target), and agent reallocation hours.

Bottom Line

Insurance email is ripe for AI automation because volume is high, categories are predictable, and integration requirements are well-defined. Build compliance into the architecture — state-specific rules, claims handling sensitivity, and policy-specific responses.

Automate the repetitive 80% of insurance emails. Robylon AI connects to your claims and policy systems to resolve status inquiries, generate COIs, and process renewals — without compliance risk. Start free at robylon.ai

FAQs

What compliance guardrails does insurance AI email need?

Essential guardrails: never make coverage determinations, include state-mandated disclosures, log all interactions for regulatory examination (3–7 year retention), and mandatory escalation for emails mentioning attorneys, DOI complaints, bad faith allegations, or fraud indicators.

What is the ROI of AI email for insurance companies?

Key metrics include claims email turnaround dropping from 24–48 hours to under 2 hours, COI generation reducing from days to minutes, renewal retention rate improvement, and agent reallocation hours to complex claims and underwriting.

How does AI handle state-by-state insurance regulations?

The AI maintains a regulatory compliance database mapping each policyholder to their state's specific rules for cancellation notices, grace periods, claims timelines, and mandatory disclosures — applying the correct framework automatically.

Can AI make coverage determinations for insurance?

No — this is a critical guardrail. AI can describe what the policy says by pulling specific endorsements and exclusions, but determining whether a particular loss is covered requires human judgment due to legal and financial consequences.

Which insurance emails can AI automate?

AI automates claims status inquiries at 75–85%, COI requests at 85–95%, renewal and billing at 60–75%, and policy coverage questions at 50–65%. Complex claims disputes, underwriting exceptions, and emails mentioning attorneys require human handling.

.png)